The British soft-fruit market is a roaring success. It has seen phenomenal growth over the past few decades, creating jobs, making the country richer, healthier and just that little bit happier. It is a case study used all over the world.

As a forecasting company with a lot of berry projects, we are keen to understand how the sector will evolve. Here we look at some of the potential upsides and downsides for the coming years. Inevitably, we begin with a few Brexit considerations, but then also consider what could be done to further accelerate the sector’s growth.

Before the UK voted to leave the EU, soft fruit was projected to reach £2.3 billion in consumer value by 2025.

Using this as a baseline, we will evaluate the impact of three factors, flexing GDP, migration and inequality. Two of these scenarios are negative, one very positive.

GDP

Until June 2016, the OBR was forecasting long-term annual GDP growth of 2.1 per cent. Their revised forecast for an “orderly” Brexit shows an average growth of 1.5 per cent per year. Based on berry consumption’s past sensitivity to GDP, this slowdown is likely to reduce the market size by £150 million per year by 2025, compared to the baseline. A more extreme scenario of flat GDP would increase this gap to over £1bn per year (as a lost opportunity). But GDP is a broad indicator, itself the result of many factors. Let’s evaluate the impact of some of the underlying changes.

Migration

There are currently 3.8m EU nationals living in the UK, spending an estimated £90m on berries each year. Among them, two groups could be particularly affected by Brexit: financial sector employees (400,000) and low-skilled workers (575,000). If a quarter of them relocate, the direct impact in berry consumption is projected at -£7.5m by 2025. The indirect impact is higher though, as when they leave they no longer buy groceries, rent flats or pay into the NHS. This small population shift alone would reduce the GDP by almost £5bn (0.25 per cent), resulting in a total projected impact on the berry market of around £50m.

An even larger impact could come on the production side. Virtually all pickers are immigrants, and a shortage of labour could cause significant disruption to the country’s production capacity. Even with a new seasonal worker scheme in place, the weaker pound and a perception of not being welcome might put off many experienced EU pickers. Possible solutions to this problem include: relocating part of the capacity outside the UK, using robotics or increasing wages. But all of these options result in higher cost, which is likely to depress demand. A seven per cent increase in production cost for the UK season is projected to reduce the long-term market value by £180m/year.

Growth opportunity

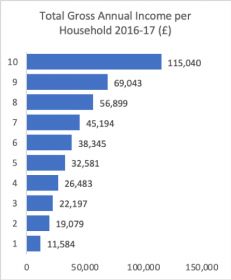

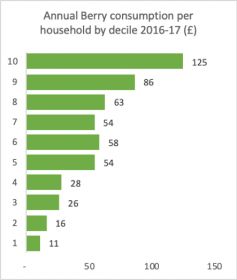

To find growth, we need to move the discussion away from Brexit. The charts on this page show income and consumption of the UK population across deciles: 10 equal groups of households ranked from (1) poorest to (10) richest. The positive scenario here is one of convergence. If living standards in the bottom four deciles were to converge just to the level of the fifth, annual berry consumption would gain more than £600m. Of course, we are not suggesting that the berry industry can single-handedly improve welfare for almost half the country’s households. What we are proposing is to bring this issue to the centre of the public debate, and work with government and other stakeholders to promote change. The aggregate value of this gap is equivalent to 11 per cent of GDP, so it will take years to narrow it down. The sooner we start, the better.

No comments yet